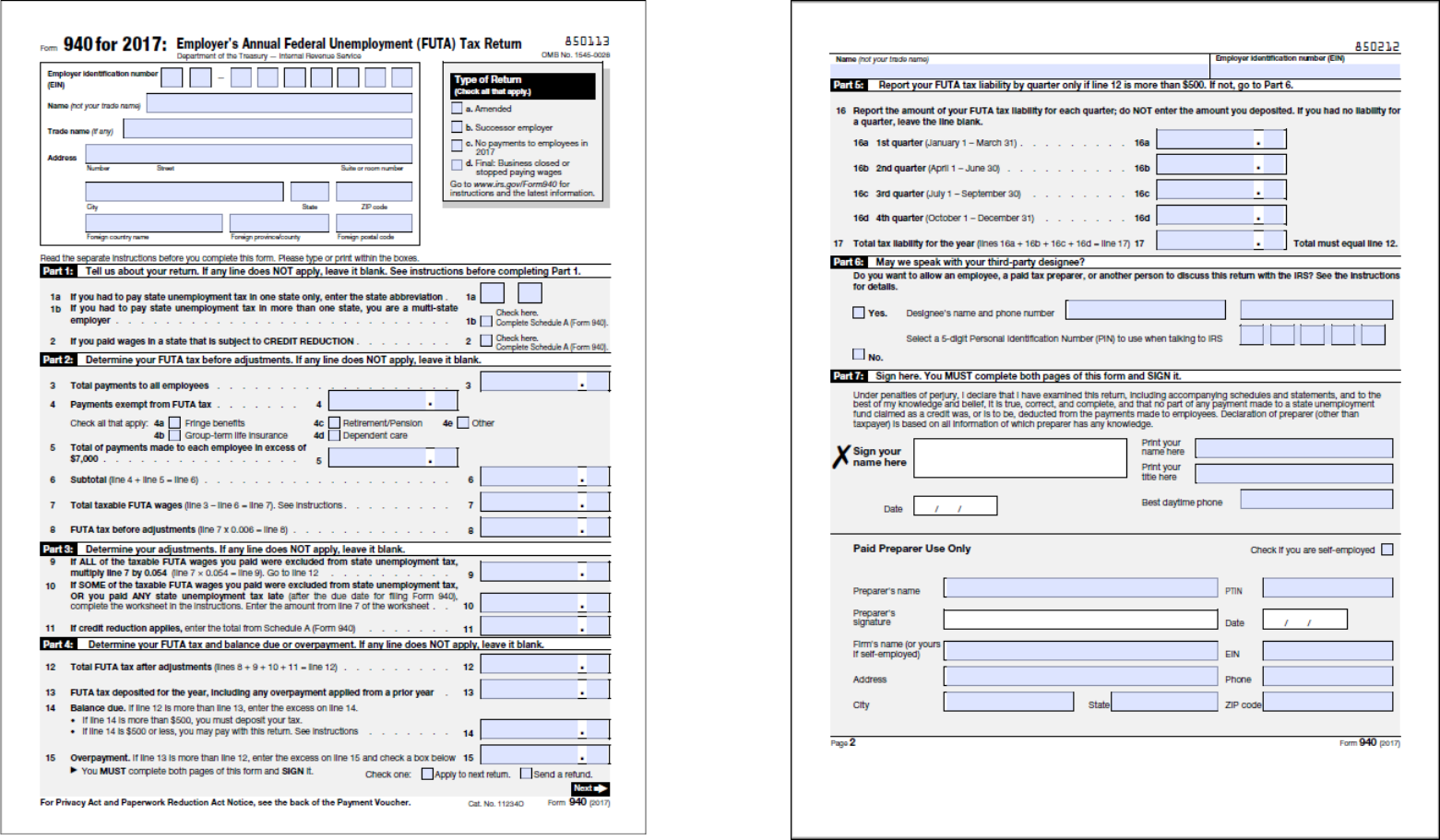

IRS FORM 940

Instructions:

Select any any line or box for IRS instructions and QuickBooks information and

troubleshooting steps.

Select Back to Form to get back to the main form.

For more information see:

• Form 940: https://www.irs.gov/pub/irs-pdf/f940.pdf

• Instructions for Form 940: https://www.irs.gov/pub/irs-pdf/i940.pdf

Back to Form

Employer Identification Number (EIN)

IRS Instructions:

Employer identification number (EIN).

An EIN is a unique nine-digit number assigned to sole proprietors, corporations, partnerships,

estates, trusts, and other entities for tax filing and reporting purposes. Businesses that need an

EIN must apply for a number and use it throughout the life of the business on all tax returns,

payments, and reports.

Your business should have only one EIN. If you have more than one and are unsure which one to

use, call 1-800-829-4933 to verify your correct EIN.

If you don't have an EIN, apply for one by:

• Visiting IRS.gov/EIN, or

• Filling out Form SS-4 and mailing it to the address in the Instructions for Form SS-4 or faxing

it to the number in the Instructions for Form SS-4.

Employers outside the United States may also apply for an EIN by calling 267-941-1099 (toll

call), but domestic entities may not apply by telephone.

If you haven't received your EIN by the time a return is due, write “Applied For” and the date

you applied in the space shown for the EIN on pages 1 and 2 of your return.

CAUTION: If you’re filing your tax return electronically, a valid EIN is required at the time the

return is filed. If a valid EIN isn't provided, the return won't be accepted. This may result in

penalties.

TIP: Always be sure the EIN on the form you file exactly matches the EIN that the IRS assigned

to your business. Don't use a social security number (SSN) or individual taxpayer identification

number (ITIN) on forms that ask for an EIN. Filing a Form 940 with an incorrect EIN or using the

EIN of another's business may result in penalties and delays in processing your return.

How QuickBooks populates this line:

QuickBooks pulls this information from the EIN (Federal Employer Identification Number)

field.

To verify your QuickBooks

• Online: Select the Gear icon > Payroll Settings > Federal Taxes. Under Federal Tax

Setup, update your EIN.

• Desktop: To change your EIN, click on Company and then on My Company. Click the

edit icon and click the Company Information tab. Enter the correct EIN in the Federal

Employer Identification Number field, and click OK. You will have to create a new

form once you've changed your company EIN.

Back to Form

Name, Trade Name, Address

IRS Instructions:

Employer Identification Number (EIN), Name, Trade Name, and Address

Enter Your Business Information at the Top of the Form Enter your EIN,

name, and address in the spaces provided. You must enter your name

and EIN here and on page 2. Enter the business (legal) name that you

used when you applied for your EIN on Form SS-4. For example, if you’re

a sole proprietor, enter “Ronald Smith” on the Name line and “Ron's

Cycles” on the Trade Name line. Leave the Trade Name line blank if it is

the same as your Name.

If you pay a tax preparer to fill out Form 940, make sure the preparer

shows your business name exactly as it appeared when you applied for

your EIN.

How QuickBooks populates this line:

• Online: QuickBooks Online pulls this information from the data provided in

the Company General Tax Information window.

• Desktop: QuickBooks Desktop pulls this information from data provided in

the Company Information window.

To verify your QuickBooks

To change the information in this section, choose My Company from the Company menu.

Make any necessary changes, and click OK.

• Online: Select the Gear icon > Payroll Settings > General Tax

information. Under Company General Tax Information update your Filing

Name and Filing Address.

• Desktop: From the Company menu, choose My Company. Click the edit icon and click

the Contact Information and Legal Information tabs to make any necessary correction

to the address, and click OK. You will have to create a new form once you've change

your company address.

Back to Form

Type of Return

IRS Instructions:

Type of Return

Review the box at the top of the form. If any line applies to you, check the appropriate box to tell us

which type of return you’re filing. You may check more than one box.

Amended. If this is an amended return that you’re filing to correct a return that you previously filed,

check box a.

Successor employer. Check box b if you're a successor employer and:

• You’re reporting wages paid before you acquired the business by a predecessor who was required to

file a Form 940 because the predecessor was an employer for FUTA tax purposes, or

• You’re claiming a special credit for state unemployment tax paid before you acquired the business by

a predecessor who wasn't required to file a Form 940 because the predecessor wasn't an employer

for FUTA tax purposes.

A successor employer is an employer who:

• Acquires substantially all the property used in a trade or business of another person (predecessor) or

used in a separate unit of a trade or business of a predecessor, and

• Immediately after the acquisition, employs one or more people who were employed by the

predecessor.

No payments to employees in 2017. If you’re not liable for FUTA tax for 2017 because you made no

payments to employees in 2017, check box c. Then go to Part 7, sign the form, and file it with the IRS.

Final: Business closed or stopped paying wages. If this is a final return because you went out of

business or stopped paying wages and you won't be liable for filing Form 940 in the future, check box d.

Complete all applicable lines on the form, sign it in Part 7, and file it with the IRS. Include a statement

showing the address at which your records will be kept and the name of the person keeping the

records.

Disregarded entities. A disregarded entity is required to file Form 940 using its name and EIN, not the

name and EIN of its owner. An entity that has a single owner and is disregarded as separate from its

owner for federal income tax purposes is treated as a separate entity for purposes of payment and

reporting federal employment taxes. If the entity doesn't currently have an EIN, it must apply for one

using one of the methods under Employer identification number (EIN), earlier. Disregarded entities

include single-owner limited liability companies (LLCs) that haven't elected to be taxed as a corporation

for federal income tax purposes, qualified subchapter S subsidiaries, and certain foreign entities treated

as disregarded entities for U.S. income tax purposes. Although a disregarded entity is treated as a

separate entity for employment tax purposes, it isn't subject to FUTA tax if it is owned by a tax-exempt

organization under section 501(c)(3) and isn't required to file Form 940. For more information, see

Disregarded entities and qualified subchapter S subsidiaries in the Introduction section of Pub. 15.

How QuickBooks populates this line:

QuickBooks does not supply this information.

Back to Form

Line 1a - Required to pay state

unemployment tax in one state only

IRS Instructions:

If You Were Required to Pay Your State Unemployment Tax In . . .

CAUTION: You must complete line 1a or line 1b even if you weren’t required

to pay any state unemployment tax because your state unemployment tax

rate(s) was zero. You may leave lines 1a and 1b blank only if all of the wages

you paid to all employees in all states were excluded from state

unemployment tax. If you leave lines 1a and 1b blank, and line 7 is more than

zero, you must complete line 9 because all of the taxable FUTA wages you

paid were excluded from state unemployment tax.

Identify the state(s) where you were required to pay state unemployment

taxes.

1a. One state only. Enter the two-letter U.S. Postal Service abbreviation for

the state where you were required to pay your state unemployment tax on

line 1a. For a list of state abbreviations, see the Schedule A (Form 940)

instructions or visit the website for the U.S. Postal Service at USPS.com.

How QuickBooks populates this line:

QuickBooks supplies the state abbreviation if you paid state

unemployment in only one state.

Back to Form

Line 1b - Required to pay state

unemployment tax in more than one state

IRS Instructions:

If You Were Required to Pay Your State Unemployment Tax In . . .

CAUTION: You must complete line 1a or line 1b even if you weren’t required to

pay any state unemployment tax because your state unemployment tax rate(s)

was zero. You may leave lines 1a and 1b blank only if all of the wages you paid to

all employees in all states were excluded from state unemployment tax. If you

leave lines 1a and 1b blank, and line 7 is more than zero, you must complete line

9 because all of the taxable FUTA wages you paid were excluded from state

unemployment tax.

Identify the state(s) where you were required to pay state unemployment taxes.

1b. More than one state (you’re a multi-state employer). Check the box on line

1b. Then fill out Schedule A (Form 940) and attach it to your Form 940.

How QuickBooks populates this line:

QuickBooks checks this box if you have accrued state unemployment taxes

in more than one state.

Back to Form

Line 2 - Paid wages in a state subject to credit

reduction

IRS Instructions:

If You Paid Wages in a State That is Subject to Credit Reduction

A state that hasn't repaid money it borrowed from the federal government to

pay unemployment benefits is called a “credit reduction state.” The U.S.

Department of Labor determines which states are credit reduction states.

If you paid wages that are subject to the unemployment tax laws of a credit

reduction state, you may have to pay more FUTA tax when filing your Form 940.

For tax year 2017, there are credit reduction states. If you paid wages subject to

the unemployment tax laws of these states, check the box on line 2 and fill out

Schedule A (Form 940). See the instructions for before completing the Schedule

A (Form 940).

How QuickBooks populates this line:

QuickBooks checks this box if you paid state unemployment in a credit

reduction state.

Back to Form

Line 3 – Total payments to all employees

IRS Instructions:

Total Payments to All Employees Report the total payments you made during the

calendar year on line 3. Include payments for all employees, even if the payments

aren't taxable for FUTA. Your method of payment doesn't determine whether

payments are wages. You may have paid wages hourly, daily, weekly, monthly, or

yearly. You may have paid wages for piecework or as a percentage of profits. Include:

• Compensation, such as: —Salaries, wages, commissions, fees, bonuses, vacation

allowances, and amounts you paid to full-time, part-time, or temporary employees.

• Fringe benefits, such as: —Sick pay (including third-party sick pay if liability is

transferred to the employer). For details on sick pay, see Pub. 15-A, Employer's

Supplemental Tax Guide. —The value of goods, lodging, food, clothing, and non-

cash fringe benefits. —Section 125 (cafeteria) plan benefits.

• Retirement/Pension, such as: —Employer contributions to a 401(k) plan, payments

to an Archer MSA, payments under adoption assistance programs, and

contributions to SIMPLE retirement accounts (including elective salary reduction

contributions). —Amounts deferred under a non-qualified deferred compensation

plan.

• Other payments, such as: —Tips of $20 or more in a month that your employees

reported to you. —Payments made by a predecessor employer to the employees of

a business you acquired. —Payments to nonemployees who are treated as your

employees by the state unemployment tax agency.

CAUION: Wages may be subject to FUTA tax even if they are excluded from your state's

unemployment tax.

For details on wages and other compensation, see section 5 of Pub. 15-A.

Example You had 3 employees. You paid $44,000 to Joan Rose, $8,000 to Sara Blue,

and $16,000 to John Green. $44,000 Amount paid to Joan 8,000 Amount paid to Sara +

16,000 Amount paid to John = $68,000 Total payments to employees. You would enter

this amount on line 3.

Back to Form

Continued on next page

Line 3 – Total payments to all employees

continued…

How QuickBooks populates this line:

From your employee's paychecks, QuickBooks totals all the payroll item types of Compensation, Reported

Tips, Dependent Care FSA, Section 457 Distribution, Non-qual. Plan Distr, Fringe Benefits, Other Moving

Expenses, 401(k), 403(b), 408(k)(6) SEP, Elective 457(b), Simple IRA, Taxable Grp Trm Life, Med Care Flex

Spend, Premium Only/125, SCorp Pd Med Premium.

To verify your QuickBooks

Online:

1. Select Reports > and search for the Payroll Details Report.

2. Filter by the Quarter and include All Employees, then click Run Report.

3. Scroll to the bottom. Review the total wages for the quarter affected.

Desktop:

1. Run a Payroll Item Listing Report.

2. Filter the report and, in the Columns, clear everything but the Payroll Item and tax-tracking type.

3. Print the report.

4. Place a check mark next to any item that has a tax-tracking type of Compensation, Reported Tips,

Dependent Care FSA, Section 457 Distribution, Non-qual. Plan Distr, Fringe Benefits, Other Moving

Expenses, 401(k), 403(b), 408(k)(6)SEP, Elective 457(b), Simple IRA, Taxable Grp Trm Life, Med Care Flex

Spend, Premium Only/125, SCorp Pd Med Premium.

5. Run a Payroll Summary report for the calendar year.

6. Click Customize Report.

7. Click the Filters tab.

8. Under Current filter choices, click Payroll Item.

9. In the drop-down box in the middle, pick Multiple Payroll Items. Check off all the payroll items you

marked earlier.

10. Add together the Adjusted Gross Pay, Total Employer Taxes, and Contributions.

If any of them are incorrect, the tax-tracking type needs to be modified.

To change a tax-tracking type:

1. Go to the Payroll Item List.

2. Double-click the payroll item in question.

3. Click Next, until you get to Tax Tracking Type.

4. Correct the tracking type and click Next until you reach Finish. This will correct the form, but if the

taxability changed, a

Payroll Checkup should be run to correct the taxable wage bases.

Back to Form

Previous page

Pro Tip:

This box will include wages paid over the annual wagebase (7000 in 2018).

Excess wages will be deducted in Box 5.

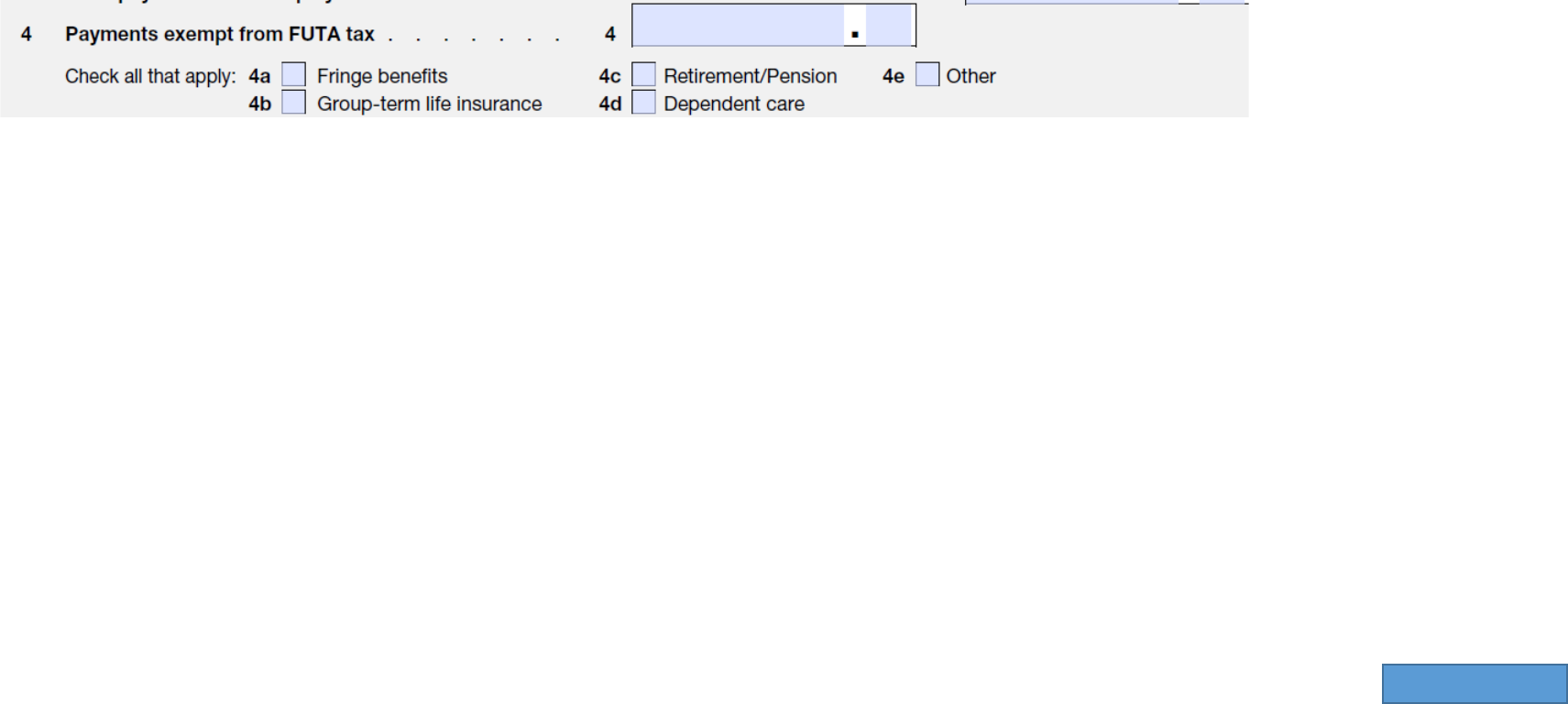

Line 4 – Payments exempt from FUTA tax

IRS Instructions:

Payments Exempt from FUTA Tax If you enter an amount on line 4, check

the appropriate box or boxes on lines 4a through 4e to show the types of

payments exempt from FUTA tax. You only report a payment as exempt

from FUTA tax on line 4 if you included the payment on line 3.

Some payments are exempt from FUTA tax because the payments aren't

included in the definition of wages or the services aren't included in the

definition of employment. Payments exempt from FUTA tax may include:

• Fringe benefits, such as:

• —The value of certain meals and lodging.

• —Contributions to accident or health plans for employees,

including certain employer payments to a Health Savings

Account or an Archer MSA.

• —Employer reimbursements (including payments to a third

party) for qualified moving expenses, to the extent that these

expenses would otherwise be deductible by the employee.

• —Payments for benefits excluded under section 125

(cafeteria) plans.

• Group term life insurance.

For information about group term life insurance and other payments

for fringe benefits that may be exempt from FUTA tax, see Pub. 15-B.

• Retirement/Pension, such as employer contributions to a qualified

plan, including a SIMPLE retirement account (other than elective

salary reduction contributions) and a 401(k) plan.

• Dependent care, such as payments (up to $5,000 per employee,

$2,500 if married filing separately) for a qualifying person's care that

allows your employees to work and that would be excludable by the

employee under section 129.

• Other payments, such as:

• —All non-cash payments and certain cash payments for agricultural

labor, and all payments to “H-2A” visa workers. See For Agricultural

Employers, earlier, or see Pub. 51.

• —Payments made under a workers' compensation law because of a

work-related injury or sickness. See section 6 of Pub. 15-A.

• —Payments for domestic services if you didn't pay cash wages of

$1,000 or more (for all domestic employees) in any calendar quarter in

2016 or 2017, or if you file Schedule H (Form 1040). See For

Employers of Household Employees, earlier, or Pub. 926.

• —Payments for services provided to you by your parent, spouse, or

child under the age of 21. See section 3 of Pub. 15. —Payments for

certain fishing activities. See Pub. 334, Tax Guide for Small Business.

• —Payments to certain statutory employees. See section 1 of Pub. 15-

A.

• —Payments to nonemployees who are treated as your employees by

the state unemployment tax agency.

See section 3306 and its related regulations for more information about

FUTA taxation of retirement plan contributions, dependent care

payments, and other payments.

For more information on payments exempt from FUTA tax, see section 15

in Pub. 15.

Example

You had 3 employees. You paid $44,000 to Joan Rose, including $2,000 in

health insurance benefits. You paid $8,000 to Sara Blue, including $500 in

retirement benefits. You paid $16,000 to John Green, including $2,000 in

health and retirement benefits.

$ 2,000 Health insurance benefits for Joan

500 Retirement benefits for Sara

+ 2,000 Health and retirement benefits for John

Equals

$4,500 Total payments exempt from FUTA tax. You would enter this

amount on line 4 and check boxes 4a and 4c.

Back to Form

Continued on next page

Line 4 – Payments exempt from FUTA tax

continued…

How QuickBooks populates this line:

In QuickBooks exempt payments are included in the total payments to all employees. They are computed from the total exempt

payments on the interview worksheet. Exempt payments include QuickBooks payroll items with the following tax tracking

types: Fringe benefits, Group Term Life Insurance, Retirement/Pension, Dependent Care, other exempt payments, and any payroll

item set to calculate before FUTA withholding. If you selected the "Federal Unemployment" tax setting for a particular payroll item,

the amount for that payroll item is calculated before FUTA withholding. QuickBooks includes the amount for that payroll item in the

Exempt Payments total.

To verify your QuickBooks

Desktop:

1. Run a Payroll Item Listing report to see the tax tracking types assigned to the payroll items in QuickBooks.

• To run a Payroll Item Listing report, go to the Reports menu, choose Employees & Payroll, and click Payroll Item Listing.

The Payroll Item Listing report displays detailed information about all defined payroll items, including their tax tracking

types. With this report, you can identify the items that impact the amount on Line 4.

• These tax tracking types are Fringe benefits, Group Term Life Insurance, Retirement/Pension, Dependent Care

2. Run a Payroll Summary report for the Form 940 filing period and note the amounts for the payroll items with the matching tax

tracking types.

• To run a Payroll Summary report, go to the Reports menu, choose Employees & Payroll, and click Payroll Summary. If

necessary, change the date range in the report window to Last Calendar Year. NOTE: You can also filter the Payroll

Summary report to show only the desired payroll items and their amounts.

Online:

1. Select Reports and search for the Payroll Details Report.

2. Filter by the Year and include All Employees, then click Run Report.

3. Scroll to the bottom. Review the total wages and deductions for the period affected, subtracting pre-tax items that are such as

401(k), pre-tax medical, fringe benefits, etc.

Back to Form

Previous page

Pro Tip:

For QuickBooks Desktop Payroll, these boxes are based

on the “tax tracking type” used in the deduction items. If

the correct box is not marked, double check the “tax

tracking type” used in those items.

Line 5 - Total of payments made to each

employee in excess of $7,000

IRS Instructions:

Total of Payments Made to Each Employee in Excess of $7,000

Only the first $7,000 you paid to each employee in a calendar year,

after subtracting any payments exempt from FUTA tax, is subject to

FUTA tax. This $7,000 is called the FUTA wage base.

Enter on line 5 the total of the payments over the FUTA wage base you

paid to each employee during 2017 after subtracting any payments

exempt from FUTA tax shown on line 4.

For examples see https://www.irs.gov/pub/irs-pdf/i940.pdf

If you’re a successor employer . . . When you figure the payments

made to each employee in excess of the FUTA wage base, you may

include the payments that the predecessor made to the employees

who continue to work for you only if the predecessor was an employer

for FUTA tax purposes resulting in the predecessor being required to

file Form 940.

How QuickBooks populates this line:

Line 5 is the total payments from line 3, less the total amount over $7,000 (the

FUTA wage base) paid to each employee during the year. If an employee received

less than the FUTA wage base during the year, the entire amount is excluded from

the amount on line 5. Exempt payments are not included in total payments.

To verify your QuickBooks

Online:

Run a Tax and Wage Summary report. In QuickBooks Online, Select Reports > and

search for the Tax and Wage Summary Report. Filter by quarter, then click Run

Report. Look for the totals under Federal Unemployment (940) . Excess wages

would listed under the column titled Excess Wages.

Desktop:

To see the amounts over the FUTA wage base, run a Payroll Item Detail report:

1. Go to the Reports menu

2. Choose Employee & Payroll, and click Payroll Item Detail. Change the date

to This Calendar Year.

3. Scroll down to Federal Unemployment.

4. The Wage Base column shows the amount subject to FUTA tax up to the $7,000

FUTA wage base.

5. To determine the amount for line 5, subtract the wage base from the amount

on line 3, total payments.

Back to Form

Line 6 - Subtotal

IRS Instructions:

Subtotal

To figure your subtotal, add the amounts on lines 4 and 5 and enter

the result on line 6.

How QuickBooks populates this line:

QuickBooks calculates the amount by adding the amount of FUTA-exempt

wages and the amount of wages over the FUTA wage base.

To verify your QuickBooks

If the amount of wages exempt from FUTA is incorrect, see the verification

instructions for line 4 and line 3.

Back to Form

Line 7 - Total taxable FUTA wages

How QuickBooks populates this line:

QuickBooks calculates the line 7 amount by subtracting the subtotal on line

6 from your total employee payments.

How to verify your QuickBooks

If the amount from line 6 or line 3 is incorrect, this line will be incorrect. See

the verification instructions for lines 3 and 4, which make up the numbers in

this calculation.

Back to Form

IRS Instructions:

Total Taxable FUTA Wages

To figure your total taxable FUTA wages, subtract line 6 from line 3

and enter the result on line 7.

Line 8 - FUTA tax before adjustments

How QuickBooks populates this line:

QuickBooks populates this amount.

To verify your QuickBooks

If the amount from line 7 is incorrect, this line will be incorrect. See the

verification instructions for lines 3 and 4, which make up the numbers in this

calculation.

Back to Form

IRS Instructions:

FUTA Tax Before Adjustments

To figure your total FUTA tax before adjustments, multiply line 7

by 0.006 and then enter the result on line 8.

Line 9 - If all taxable FUTA wages were

excluded

Pro Tip:

The IRS offers a tax credit to employers who pay state unemployment

tax of 5.4%. If the entire company is exempt from state

unemployment tax then they are subject to the full FUTA rate of 6.0%.

If Line 9 applies to you, lines 10 and 11 don’t apply to you.

Back to Form

IRS Instructions:

If ALL of the Taxable FUTA Wages You Paid Were Excluded from State

Unemployment Tax . . .

CAUTION: Line 9 doesn't apply to FUTA wages on which you paid no state

unemployment tax only because the state assigned you a tax rate of zero percent.

If all of the taxable FUTA wages you paid were excluded from state unemployment

tax, multiply line 7 by 0.054 and enter the result on line 9.

If you weren't required to pay state unemployment tax because all of the wages

you paid were excluded from state unemployment tax, you must pay FUTA tax at

the 6.0% (0.060) rate. For example, if your state unemployment tax law excludes

wages paid to corporate officers or employees in specific occupations, and the

only wages you paid were to corporate officers or employees in those specific

occupations, you must pay FUTA tax on those wages at the full FUTA rate of 6.0%

(0.060). When you figured the FUTA tax before adjustments on line 8, it was based

on the maximum allowable credit (5.4%) for state unemployment tax payments.

Because you didn't pay state unemployment tax, you don't have a credit and must

figure this adjustment.

If line 9 applies to you, lines 10 and 11 don't apply to you. Therefore, leave lines

10 and 11 blank. Don't fill out the worksheet in these instructions. Complete

Schedule A (Form 940) only if you’re a multi-state employer.

Continued on next page

Line 9 - If all taxable FUTA wages were excluded

continued…

How QuickBooks populates this line:

If all wages you paid to employees were not subject to state unemployment tax (as

defined in your setup interview), QuickBooks Desktop adds them together and multiplies

that amount by .054.

If there is a value for line 9, QuickBooks will not figure a value for lines 10 and 11.

To verify your QuickBooks

Online

Run a Tax and Wage Summary report. In QuickBooks Online, Select Reports > and search

for the Tax and Wage Summary Report. Filter by quarter, then click Run Report. Look for

the totals under Federal Unemployment (940) . Excess wages would listed under the

column titled Excess Wages.

Desktop:

If this figure is incorrect, you may have incorrectly set up the tax-tracking type of one or

more of payroll items.

1. Run a Payroll Item Listing Report.

2. Filter the report and, in the Columns, clear everything but the Payroll Item and Tax

Tracking type.

3. Print the report.

4. Put a check mark next to any item that has a tax tracking of Compensation, Filter

Reported Tips, Dependent Care FSA, Section 457 Distribution, Non-qual. Plan Distr,

Fringe Benefits, Other Moving Expenses, 401(k), 403(b), 408(k)(6)SEP, Elective 457(b),

Simple IRA, Taxable Grp Trm Life, Med Care Flex Spend, Premium Only/125, SCorp Pd

Med Premium.

5. Run a Payroll Summary report for the calendar year.

6. Click Customize Report.

7. Click the Filters tab.

8. Under Current filter choices, click Payroll Item.

9. In the drop-down box in the middle, pick Multiple Payroll Items. Check off all the

payroll items you marked earlier. If any of them are incorrect, the tax-tracking type

needs to be modified.

To change a tax-tracking type:

1. Go to the Payroll Item List.

2. Double-click the payroll item in question.

3. Click Next until you get to Tax-Tracking Type.

4. Correct the tracking type and click Next until you reach Finish. This will correct the

form, but if the taxability changed, you should run a Payroll Checkup to correct the

taxable wage bases.

Back to Form

Previous Page

Line 10 - If some taxable FUTA wages were

excluded or state unemployment tax paid late

Back to Form

IRS Instructions:

If SOME of the Taxable FUTA Wages You Paid Were Excluded From State Unemployment Tax, or

You Paid any State Unemployment Tax Late . . .

You must fill out the worksheet on the next page if:

• Some of the taxable FUTA wages you paid were excluded from state unemployment tax, or

• Any of your payments of state unemployment tax were late.

The worksheet takes you step by step through the process of figuring your credit. At the end of the

worksheet you'll find an example of how to use it. Don't complete the worksheet if line 9 applied to

you (see the instructions for line 9, earlier).

Before you can properly fill out the worksheet, you will need to gather the following information.

• Taxable FUTA wages (Form 940, line 7).

• Taxable state unemployment wages (state and federal wage bases may differ).

• The experience rates assigned to you by the states where you paid wages.

• The amount of state unemployment taxes you paid on time. (On time means that you paid the

state unemployment taxes by the due date for filing Form 940.)

• The amount of state unemployment taxes you paid late. (Late means after the due date for filing

Form 940.)

CAUTION: Don't include any penalties, interest, or unemployment taxes deducted from your

employees' pay in the amount of state unemployment taxes. Also, don't include as state

unemployment taxes any special administrative taxes or voluntary contributions you paid to get a

lower assigned experience rate or any surcharges, excise taxes, or employment and training taxes.

(These items are generally listed as separate items on the state's quarterly wage report.)

For line 3 of the worksheet:

• If any of the experience rates assigned to you were less than 5.4% for any part of the calendar

year, you must list each assigned experience rate separately on the worksheet.

• If you were assigned six or more experience rates that were less than 5.4% for any part of the

calendar year, you must use another sheet to figure the additional credits and then include those

additional credits in your line 3 total.

After you complete the worksheet, enter the amount from line 7 of the worksheet on Form 940, line

10. Don't attach the worksheet to your Form 940. Keep it with your records.

See

https://www.irs.gov/pub/irs-pdf/i940.pdf for the worksheet.

Continued on next page

Line 10 - If some taxable FUTA wages were

excluded or state unemployment tax paid late

continued…

How QuickBooks populates this line:

If you answer "YES" on part 3 of the QuickBooks Form 940 interview to the statement

that some wages were exempt from state unemployment or that state unemployment

was paid late, QuickBooks calculates the amount for line 7 of the 940 worksheet.

If there was a value calculated for line 9, QuickBooks does not enter an amount for line

10.

If there was no value for line 9, QuickBooks adds together all wages paid that have a

FUTA-taxable tax-tracking type.

To verify your QuickBooks

Online:

To verify result, check worksheet that is offered along with your 940.

Desktop

If any state unemployment taxes were paid late, fill out the worksheet in the Interview,

and QuickBooks will enter the amount from line 7 of the worksheet onto line 10 of the

Form 940.

Back to Form

Previous Page

Line 11 - If credit reduction applies

How QuickBooks populates this line:

In calculating the amount for line 2a (which is also entered on line 3) of Schedule A, QuickBooks does the following:

• If you only paid wages in credit reduction states, QuickBooks enters the total taxable FUTA wages.

• If you paid wages in one of the credit reduction states and in additional states, QuickBooks calculates this amount by allocating

the credit reduction states' SUI wages applicable to FUTA.

To verify your QuickBooks

There are two scenarios in which QuickBooks might overstate this amount:

1. If you have employees that are not subject to SUI in one of the credit reduction states but are subject to FUTA, you should not

include these wages on line 2a of Schedule A.

2. If you have employees that made less than $9,000 in a credit reduction state, the amount on line 2a may be overstated

because QuickBooks allocates wages based on total wages paid by the company, and you will need to recalculate it and adjust

the amount on line 2a of Schedule A.

Online:

To verify result, Run the Tax and Wage Summary for the year and verify wage amount.

Desktop

To verify your employee wages for a credit reduction state run a Payroll Item Detail report in QuickBooks Desktop:

1. From the Report menu, choose Employee & Payroll, and click Payroll Item Detail.

2. On the Display tab, verify that the Report Date Rate includes the date ranges for the current calendar year.

3. Click the Filters tab. In the Choose Filter section, click Payroll Item in the Filter drop-down.

4. In the Payroll Item drop-down, select Multiple payroll items, and then select Federal Unemployment and XX-Unemployment

Company, where XX is the abbreviation for each credit reduction state.

5. Click OK twice.

Back to Form

IRS Instructions:

If Credit Reduction Applies . . .

If you paid FUTA taxable wages that were also subject to state

unemployment taxes in any states that are subject to credit

reduction, enter the total amount from Schedule A (Form 940) on

Form 940, line 11. However, if you entered an amount on line 9

because all the FUTA taxable wages you paid were excluded from

state unemployment tax, skip line 11 and go to line 12.

Line 12 - Total FUTA tax after adjustments

How QuickBooks populates this line:

QuickBooks calculates this amount by adding together the amounts

for lines 8, 9, 10, and 11.

To verify your QuickBooks

If the amount from line 8, 9 10, or 11 is incorrect, this box will be

incorrect. See the verification instructions for boxes 8, 9, 10, and 11

which make up the numbers in this calculation.

Back to Form

IRS Instructions:

Total FUTA Tax After Adjustments

Add the amounts shown on lines 8, 9, 10, and 11, and enter the result

on line 12.

CAUTION: If line 9 is greater than zero, lines 10 and 11 must be zero

because they don't apply.

Line 13 - FUTA tax deposited for the year

Back to Form

IRS Instructions:

Enter the amount of FUTA tax that you

deposited for the year, including any

overpayment that you applied from a prior

year.

How QuickBooks populates this line:

QuickBooks calculates the total of FUTA payments processed during the filing period prior

to creating this form.

To verify your QuickBooks

If this number is incorrect, you can check your FUTA payments.

Online: In you QuickBooks Online program, from the left, select Taxes > Payroll

Tax. Choose the Tax Payments tab. Look for the Federal Unemployment (940) amount.

Desktop

1. Run a Payroll Liability Balances Report by going to the Reports drop-down menu,

selecting Employees & Payroll and clicking Payroll Liability Balances.

2. Change the date range to January 1 through December 31.

3. Double-click the total for Federal Unemployment. Your report will now reflect

Transactions by Payroll Liability.

4. Click Customize Report.

5. Click the Filters tab and choose Transaction Type from the scroll box.

6. Click the Transaction Type drop-down menu and choose Payroll Liability Check.

7. To see a list of transactions that make up an amount, double-click the amount.

Line 14 - Balance Due

Back to Form

IRS Instructions:

Balance Due

If line 13 is less than line 12, enter the difference on line 14.

If line 14 is:

• More than $500, you must deposit your tax. See When Must You Deposit Your FUTA

Tax, earlier.

• $500 or less, you can deposit your tax, pay your tax with a credit card or debit card, pay

your tax by EFW if filing electronically, or pay your tax by check or money order with

your return. For more information on electronic payment options, go to

IRS.gov/Payments.

• Less than $1, you don't have to pay it.

CAUTION: If you don't deposit as required and pay any balance due with Form 940, you

may be subject to a penalty. If you pay by EFT, credit card, or debit card, file your return

using the Without a payment address under Where Do You File, earlier. Don't file Form

940-V, Payment Voucher.

What if you can't pay in full? If you can't pay the full amount of tax you owe, you can

apply for an installment agreement online. You can apply for an installment agreement

online if:

• You can't pay the full amount shown on line 14,

• The total amount you owe is $25,000 or less, and

• You can pay the liability in full in 24 months.

To apply using the Online Payment Agreement Application, go to IRS.gov/OPA.

Under an installment agreement, you can pay what you owe in monthly installments.

There are certain conditions you must meet to enter into and maintain an installment

agreement, such as paying the liability within 24 months, and making all required

deposits and timely filing tax returns during the length of the agreement.

If your installment agreement is accepted, you will be charged a fee and you will be

subject to penalties and interest on the amount of tax not paid by the due date of the

return.

How QuickBooks populates this line:

Line 14 is based on the Tax Liability Payments entered into

QuickBooks for the tax period prior to creating this form.

To verify your QuickBooks

If the amount from line 12 or 13 is incorrect, this line will be

incorrect. See the verification instructions for lines 12 and 13,

which make up the numbers in this calculation.

Line 15 - Overpayment

How QuickBooks populates this line:

If line 13 is more than line 12, QuickBooks enters the result here.

To verify your QuickBooks

If the amount from line 12 or 13 is incorrect, this line will be incorrect.

See the verification instructions for lines 12 and 13, which make up the

numbers in this calculation.

Back to Form

IRS Instructions:

Overpayment

If line 13 is more than line 12, enter the difference on line 15.

If you deposited more than the FUTA tax due for the year, you may

choose to have us either:

• Apply the refund to your next return, or

• Send you a refund.

Check the appropriate box on line 15 to tell us which option you select.

Check only one box on line 15. If you don’t check either box or if you

check both boxes, generally we will apply the overpayment to your next

return. Regardless of any box you check or don’t check, we may apply

your overpayment to any past due tax account that is shown in our

records under your EIN.

If line 15 is less than $1, we will send you a refund or apply it to your next

return only if you ask for it in writing

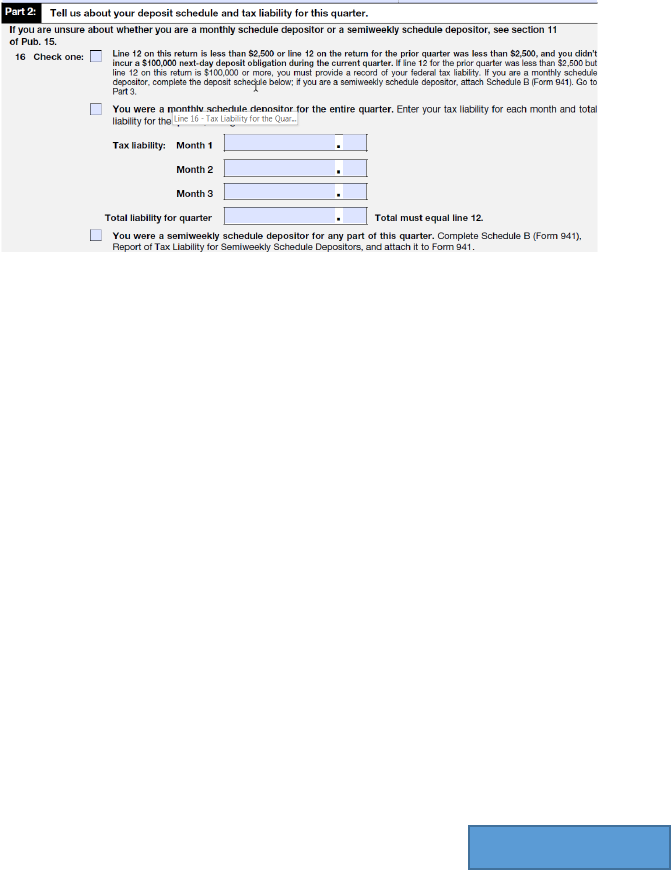

Line 16 - FUTA tax liability for each quarter

Back to Form

IRS Instructions:

Report the Amount of Your FUTA Tax Liability for Each Quarter

Enter the amount of your FUTA tax liability for each quarter on lines 16a–d. Don't enter the amount you deposited. If you had no

liability for a quarter, leave the line blank.

• 16a. 1st quarter (January 1 to March 31)

• 16b. 2nd quarter (April 1 to June 30)

• 16c. 3rd quarter (July 1 to September 30)

• 16d. 4th quarter (October 1 to December 31)

To figure your FUTA tax liability for the fourth quarter, complete Form 940 through line 12. Then copy the amount from line 12

onto line 17. Lastly, subtract the sum of lines 16a through 16c from line 17 and enter the result on line 16d.

Example: You paid wages on March 28 and your FUTA tax on those wages was $200. You weren't required to make a deposit for

the 1st quarter because your accumulated FUTA tax was $500 or less. You paid additional wages on June 28 and your FUTA tax on

those wages was $400. Because your accumulated FUTA tax for the 1st and 2nd quarters exceeded $500, you were required to

make a deposit of $600 by July 31.

You would enter $200 in line 16a because your liability for the 1st quarter is $200. You would also enter $400 in line 16b to show

your 2 nd quarter liability.

TIP: In years when there are credit reduction states, you must include liabilities owed for credit reduction with your fourth

quarter deposit. You may deposit the anticipated extra liability throughout the year, but it isn't due until the due date for the

deposit for the fourth quarter, and the associated liability should be recorded as being incurred in the fourth quarter.

Continued on next page

Line 16 - Tax Liability for the Quarter

continued…

How QuickBooks populates this line:

If your Federal Unemployment Liabilities were $500 or less, QuickBooks leaves

this part blank. Otherwise, QuickBooks calculates the amounts based on the

amount of Federal Unemployment on paychecks.

How to verify your QuickBooks

Online: Run a Tax and Wage Summary report. In QuickBooks Online,

Select Reports > and search for the Tax and Wage Summary Report. Filter by

quarter, then click Run Report. Look for the totals under Federal

Unemployment (940) . Select FUTA Employer. Change the Date Range to the

quarter you want to verify. Review the total Tax Amount.

Desktop

To find out what each quarter's Federal Unemployment was:

1. Go to the Reports menu and select Employees & Payroll.

2. Select Payroll Summary.

3. Click Customize Report.

4. Set the date range to the calendar year.

5. Set the columns to Quarter.

6. Click Filters, and under Current Filter Choices, select Payroll Item.

7. Under the Payroll Item drop-down, select Federal Unemployment.

8. Click OK.

Back to Form

Previous page

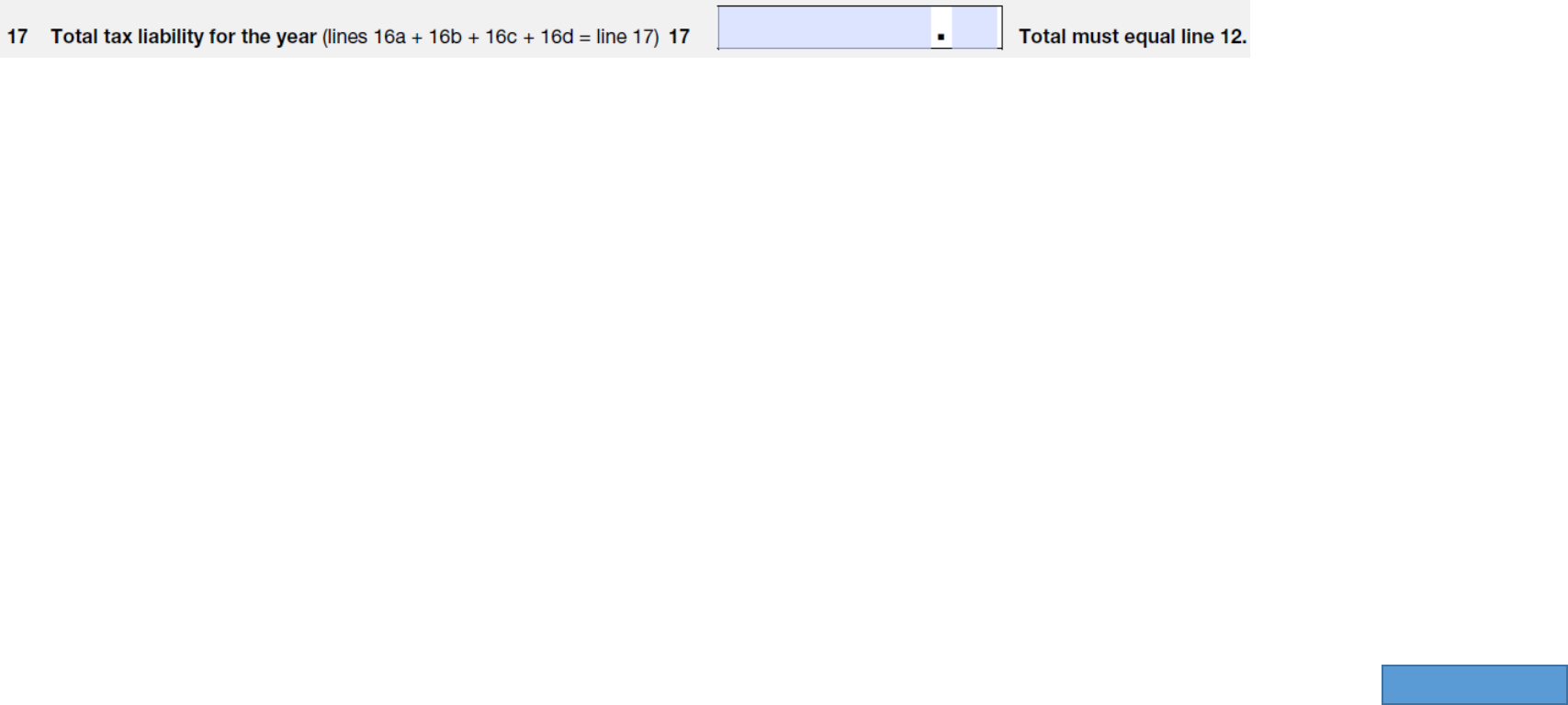

Line 17 - Total tax liability for the year

How QuickBooks populates this line:

QuickBooks enters the same figure in lines 12 and 17.

To verify your QuickBooks

If the amount from line 8, 9, 10, or 11 is incorrect, this box will be incorrect. See the

verification instructions for boxes 8, 9, 10, and 11, which make up the numbers in this

calculation.

Back to Form

IRS Instructions:

Your total tax liability for the year must equal line 12. Copy the

amount from line 12 onto line 17.

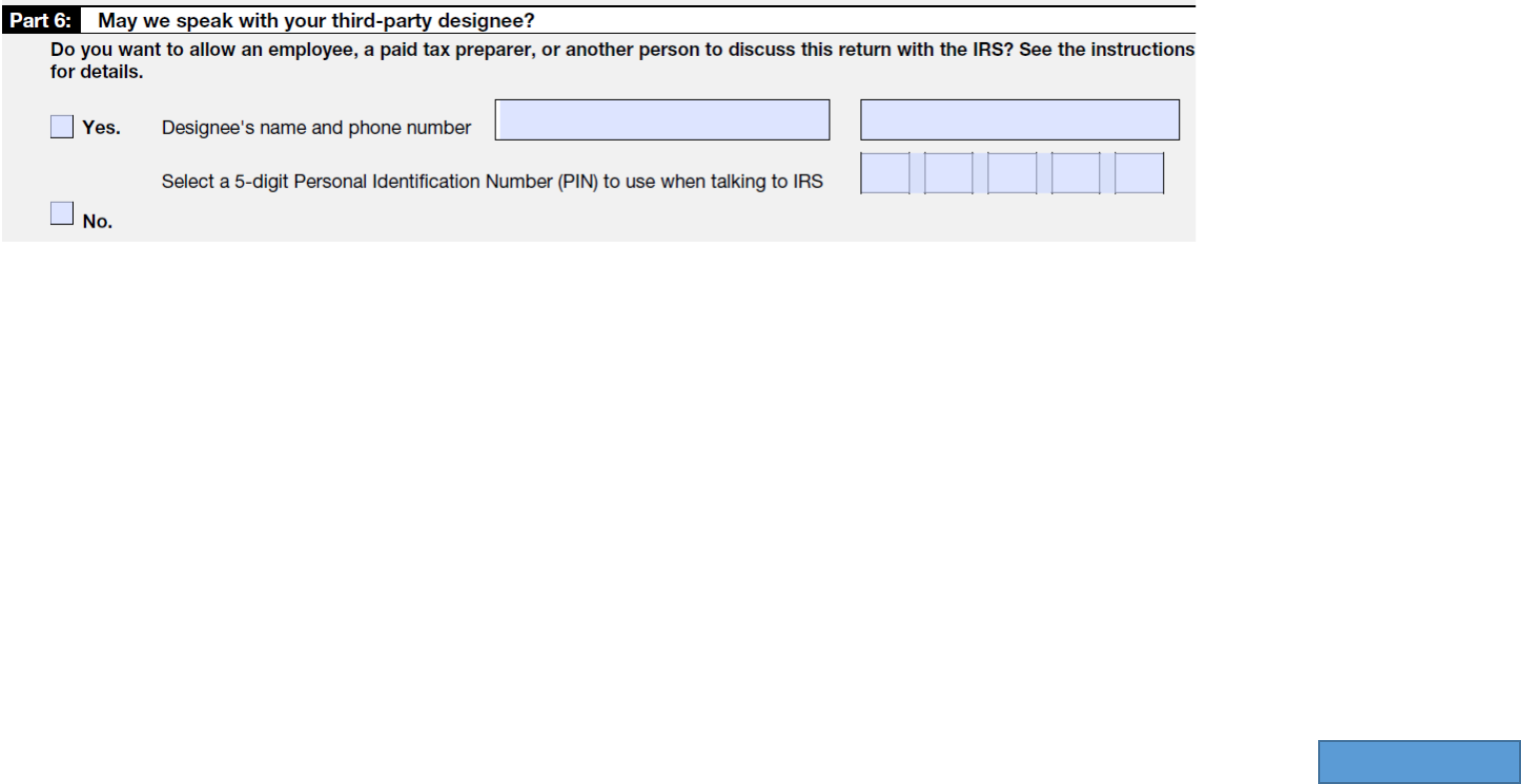

Part 6- Third-party designee

Back to Form

IRS Instructions:

May We Speak With Your Third-Party Designee?

If you want to allow an employee, your paid tax preparer, or another person to discuss your Form 940 with the IRS, check the “Yes” box. Then enter the name and phone number of the

person you choose as your designee. Be sure to give us the specific name of a person — not the name of the firm that prepared your tax return.

Have your designee select a five-digit Personal Identification Number (PIN) that he or she must use as identification when talking to the IRS about your form.

By checking “Yes,” you authorize us to talk to your designee about any questions that we may have while we process your return. Your authorization applies only to this form, for this year; it

doesn't apply to other forms or other tax years.

You’re authorizing your designee to:

• Give us any information that is missing from your return,

• Ask us for information about processing your return, and

• Respond to certain IRS notices that you have shared with your designee about math errors and in preparing your return. We won't send notices to your designee.

You’re not authorizing your designee to:

• Receive any refund check,

• Bind you to anything (including additional tax liability), or

• Otherwise represent you before the IRS.

The authorization will automatically expire 1 year after the due date for filing your Form 940 (regardless of extensions). If you or your designee want to end the authorization before it

expires, write to the IRS office for your location using the Without a payment address under Where Do You File, earlier.

If you want to expand your designee's authorization or if you want us to send your designee copies of your notices, see Pub. 947.

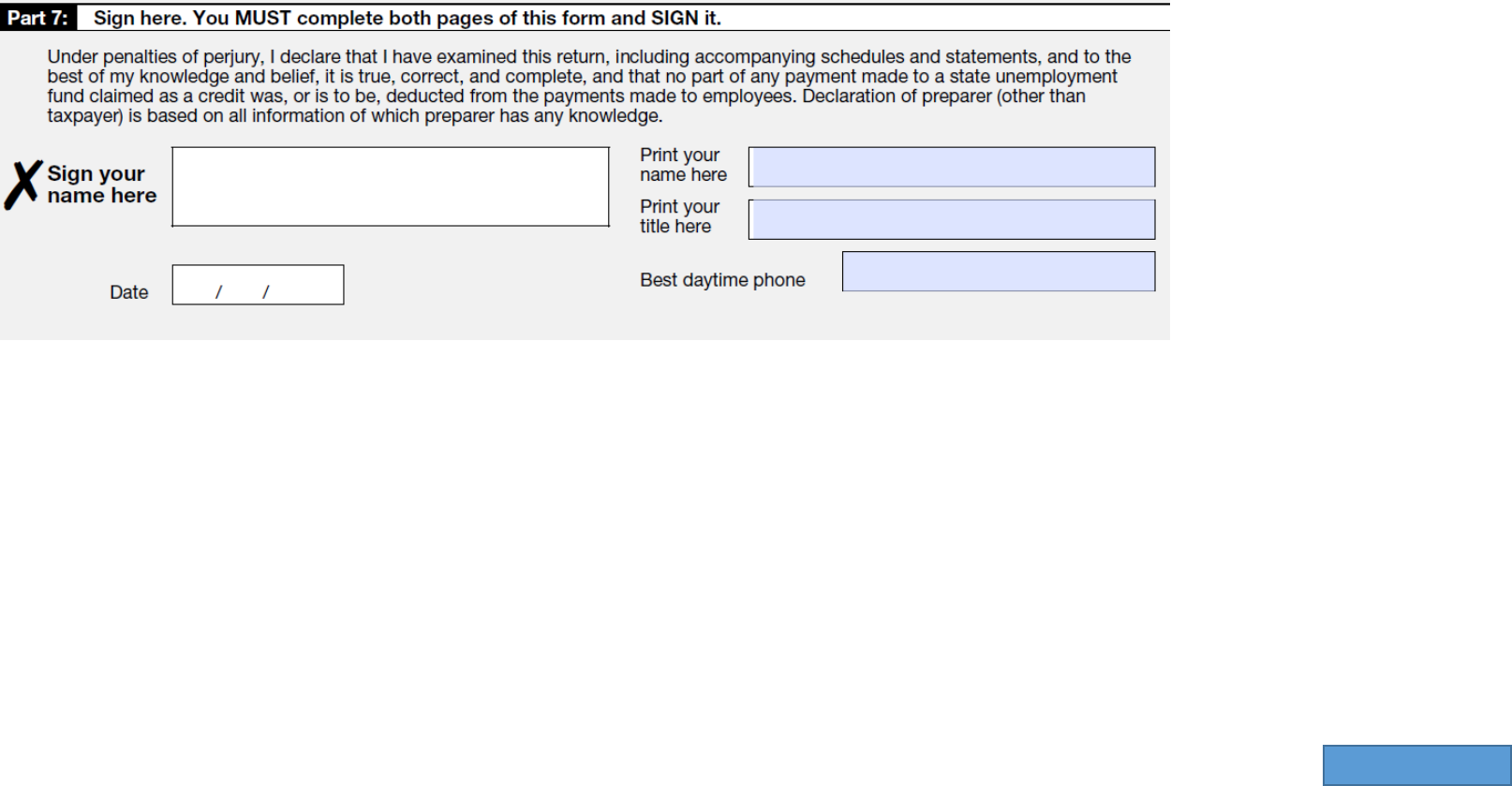

Part 7: Signature

Back to Form

IRS Instructions:

Sign Here (Approved Roles)

You MUST Fill Out Both Pages of This Form and SIGN It Failure to sign will delay the

processing of your return. On page 2 in Part 7, sign and print your name and title. Then

enter the date and the best daytime telephone number, including area code, where we

can reach you if we have any questions.

Who Must Sign Form 940? The following persons are authorized to sign the return for

each type of business entity.

• Sole proprietorship—The individual who owns the business.

• Partnership (including a limited liability company (LLC) treated as a partnership) or

unincorporated organization— A responsible and duly authorized partner, member,

or officer having knowledge of its affairs.

• Corporation (including an LLC treated as a corporation) —The president, vice

president, or other principal officer duly authorized to sign.

• Single-member LLC treated as a disregarded entity for federal income tax purposes

— The owner of the LLC or a principal officer duly authorized to sign.

• Trust or estate — The fiduciary.

Form 940 may also be signed by a duly authorized agent of the taxpayer if a valid power

of attorney or reporting agent authorization (Form 8655) has been filed.

Alternative signature method. Corporate officers or duly authorized agents may sign

Form 940 by rubber stamp, mechanical device, or computer software program. For

details and required documentation, see Rev. Proc. 2005-39, 2005-28 I.R.B. 82, available

at IRS.gov/irb/2005-28_IRB/ar16.html.

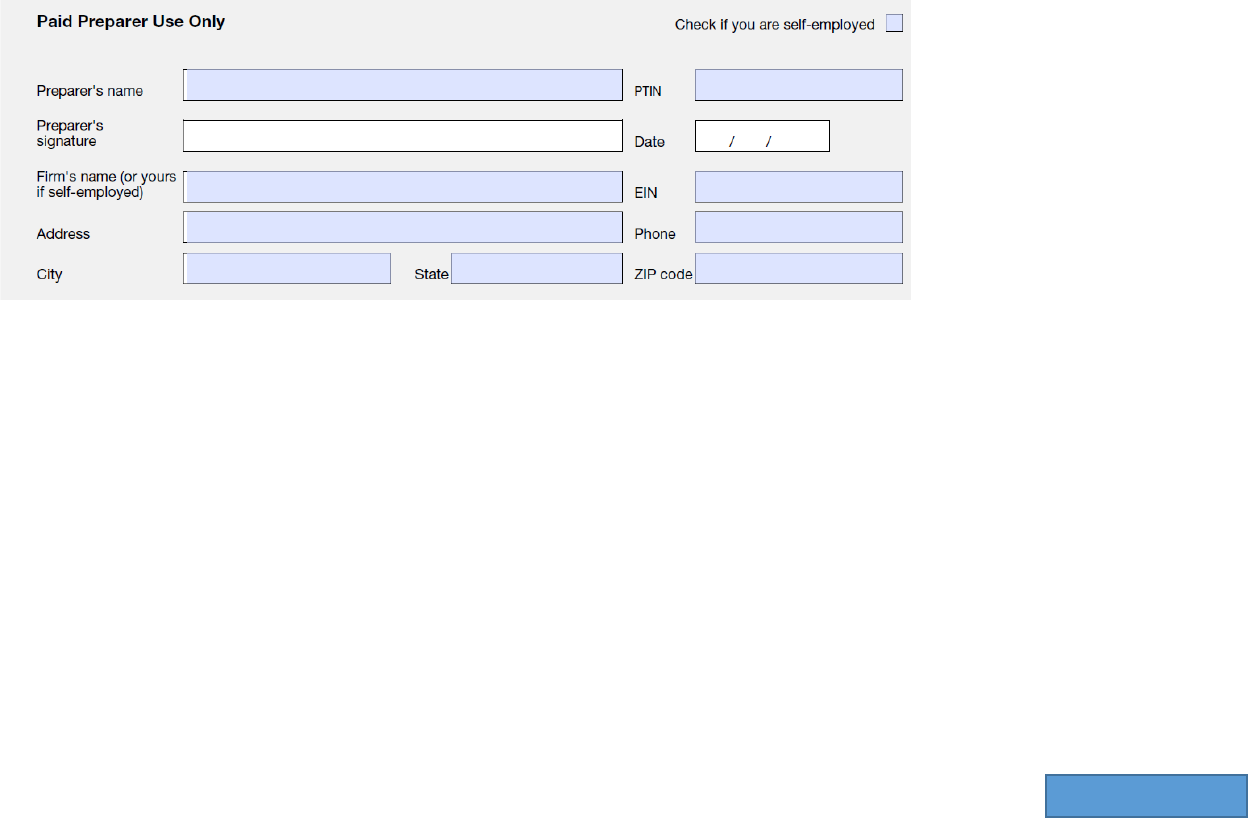

Paid Preparer Use Only

Back to Form

IRS Instructions:

Paid preparers.

A paid preparer must sign Form 940 and provide the information in the Paid Preparer Use Only section of Part 7 if the preparer was paid to

prepare Form 940 and isn't an employee of the filing entity. Paid preparers must sign paper returns with a manual signature. The preparer

must give you a copy of the return in addition to the copy to be filed with the IRS.

If you’re a paid preparer, enter your Preparer Tax Identification Number (PTIN) in the space provided. Include your complete address. If you

work for a firm, write the firm's name and the EIN of the firm. You can apply for a PTIN online or by filing Form W-12. For more information

about applying for a PTIN online, visit the IRS website at IRS.gov/PTIN. You can't use your PTIN in place of the EIN of the tax preparation firm.

Generally, don't complete the Paid Preparer Use Only section if you’re filing the return as a reporting agent and have a valid Form 8655 on file

with the IRS. However, a reporting agent must complete this section if the reporting agent offered legal advice, for example, by advising the

client on determining whether its workers are employ